Plans announced last month by a private Chinese group to revive the multi-billion dollar Oakajee port project add a new twist to a 45-year saga.

Plans announced last month by a private Chinese group to revive the multi-billion dollar Oakajee port project add a new twist to a 45-year saga. This article is the latest in our series marking our 25-year anniversary.

A new deepwater port has long been considered the key to opening up the development of Western Australia’s Mid West.

The area holds vast deposits of iron ore and other minerals, but is serviced by a single port heavily constrained by its location next to Geraldton’s city centre and unable to accept large Cape-class vessels.

Oakajee, a windswept spot about 20 kilometres north of Geraldton, was identified as the preferred site for a new port back in 1972.

One year later, the Labor government led by premier John Tonkin struck a deal with the first of many companies hoping to open up the region’s iron ore reserves.

The Iron Ore (Murchison) Authorisation Agreement Act 1973 was designed to help the now long-forgotten Northern Mining Corporation develop a new port-and-rail link to planned iron ore mines.

The state agreement subsequently passed to Kingstream Steel, which spent all of the 1990s working on its plans for a steel mill.

Chaired by Ken Court, brother of then WA premier Richard Court, and led by chief executive Nick Zuks, Kingstream had backing from Taiwan’s An Feng Steel Co.

It initially intended to develop a small-scale project that would use the existing Geraldton port, but was urged to think big and pursue a larger project that would underpin development of the new port at Oakajee.

A Business News article from March 25, 2010.

While the ambitious proposal initially raised hopes in the region, the 1997 Asian Financial Crisis and resultant collapse in steel prices doomed the project as An Feng reined-in its growth plans.

Kingstream went into administration in 2001 but re-emerged two years later after a major financial restructuring as Midwest Corporation.

Midwest and Murchison Metals, which was founded in 1997, were some of the Perth-based ASX stocks that rode the iron ore boom during the 2000s.

Each had ambitious plans – Midwest wanted to develop the giant Weld Range deposit, while Murchison sought to develop the Jack Hills mine.

The key problem for both projects was their remote location, more than 500km from the coast.

However, that issue was overcome as both companies gained heavyweight backing in the midst of the China-fuelled iron ore boom.

Japan’s Mitsubishi Corporation partnered with Murchison, and China’s Sinosteel Corporation outlaid $1.2 billion to take over Midwest Corp in 2007.

This takeover arguably signalled the high point of ‘China Inc’ paying too much for Australian assets during the boom years.

Around the same time, another Chinese steel maker, Ansteel, was partnering with ASX-listed Gindablie Metals to build the $3 billion Karara iron ore project, inland from Geraldton.

In addition, there were several other groups seeking to develop smaller iron ore projects in the region.

Collectively, these projects were capable of producing more than 50 million tonnes of iron ore per year.

That’s well above the capacity of Geraldton port, which handled 15.9mt of goods in the year to June 2018, including 12mt of iron ore.

The solution was Oakajee.

Two bidders

At the peak of the boom in 2007, two consortia were competing to develop the new port and associated rail lines.

Their backers added a geopolitical overtone to the commercial bidding.

Yilgarn Infrastructure was backed by Chinese interests and was closely aligned with Sinosteel Midwest.

At one stage it claimed the 1973 state agreement, still held by Midwest, gave it the right to develop Oakajee, but that idea was quickly shot down by the state government, which said the agreement was well past its use-by date.

Business News article from 2007.

Japan’s Mitsubishi was backing the competing Oakajee Port and Rail consortium.

In July 2008, the Labor government of Alan Carpenter selected OPR as its preferred proponent to develop Oakajee.

The early signs were promising.

In mid 2009, Ansteel said it planned to investigate the viability of a steel mill at Oakajee.

In early 2010, Sinosteel Midwest, Gindalbie Metals and Crosslands Resources – a joint venture between Murchison Metals and Mitsubishi – were selected as potential foundation customers of the port.

However, planning for the port ran up against multiple challenges.

One issue was that the Chinese groups were wary of dealing with an infrastructure provider that was aligned with both Japan and a competing miner.

Another issue was cost, which blew out from an estimated $2 billion initially to more than $4 billion.

Layered on top of that was the softening of the global iron ore market.

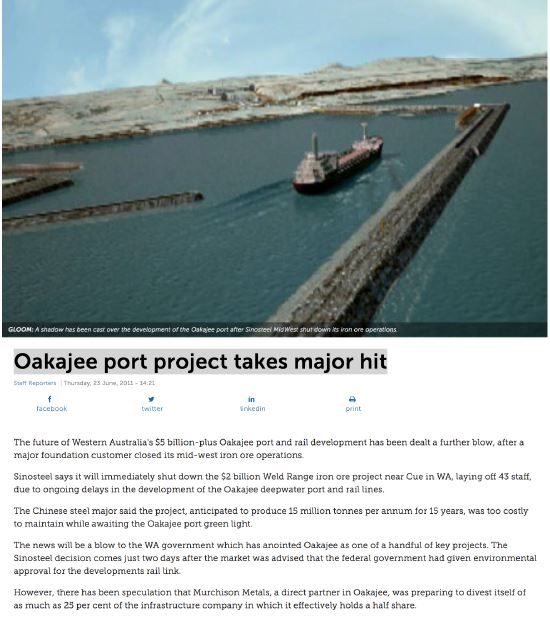

The doubts over the project escalated in June 2011 when Sinosteel halted development of its $2 billion Weld Range iron ore project.

Sinosteel said its mine, anticipated to produce 15mt annually, was too costly to maintain while awaiting the Oakajee port green light.

Business News article from 2011.

In late 2011, Mitsubishi bought Murchison Metals out of the port-and-rail project.

This was more of a last ditch effort to keep the project alive than a sign of confidence it would proceed.

As the iron ore market continued to weaken, Mitsubishi wound back its funding for OPR during 2012 and halted work on the project entirely in June 2013.

Oakajee was back in the news less than a year later, but this time for all the wrong reasons.

Little-known Perth company Padbury Mining had been quietly working on Oakajee after acquiring intellectual property and engineering studies from Yilgarn Infrastructure in 2011.

It stunned the market in 2014 when it claimed to have lined up more than $6 billion of funding to revive the port-and-rail project.

Padbury, led by former state government executive Gary Stokes, suffered a fatal credibility blow when it emerged its mystery funder was an Australian business figure with a chequered history – hair regrowth entrepreneur Roland Bleyer.

Less than three weeks after announcing the deal, Padbury terminated its so-called funding agreement.

Business News article from 2014.

Padbury subsequently went through a major restructure and emerged with new directors and a new name – AustSino Resources Group.

AustSino was at the centre of last month’s surprise announcement that a little-known Chinese group was planning to invest $100 million in Oakajee and other iron ore projects.

The Chinese investor was a private sector company named Western Australian Port Rail Construction (WAPRC).

Its major shareholders are Shanghai-based investors Li Ping and Qiu Yu Hu, who according to AustSino are involved in businesses within the industrial, property and technology sectors.

WAPRC plans to acquire a 61 per cent stake and effective control of AustSino via the purchase of 7.6 billion shares at 1.3 cents each.

Using the proceeds of the WAPRC placement, AustSino plans to acquire a majority stake in Perth-based Sundance Resources, which has been seeking to develop the Mbalam Nabeba project in Cameroon.

AustSino also plans to invest in its iron ore tenements in the Mid West, including the Peak Hill deposit, about 650km north-east of Geraldton, and undertake engineering studies at Oakajee.

This followed the announcement in May that AustSino had hired Churchill Consulting to prepare a concept study looking at infrastructure solutions for the Mid West.

Boutique advisory firm Contour Capital, led by former KPMG partner Duncan Calder, is also working for AustSino.

“The company believes the time is right to re-evaluate previous options and scenarios and to explore fresh ideas which may assist in finally developing a viable economic infrastructure solution for the region,” AustSino stated.

The West Perth-based company said its preferred model would be for its proposed project partners to directly fund the development of port and rail infrastructure under a ‘build own operate transfer’ model and to recover the cost via tariffs paid by mining companies.

It concluded by saying there was no certainty this would happen.