ASX-listed gold developer, Crusader Resources, is now back on track at its fully-owned Borborema gold project in the state of Rio Grande do Norte in north-eastern Brazil and the Perth based ASX listed company is edging ever closer to moving first dirt at the project.

Crusader recently put a broom through its management structure and it is now busy putting the finishing touches on a funding package to push forward the development of its flagship gold project in South America.

In March, the company appointed well-respected mining industry veteran Andrew Richards as Executive Director and also recently delisted from AIM, with the resignation of all existing UK Directors.

Mr Richards has worked extensively in gold, base metals, rare earths and industrial metals worldwide and will now steer the day to day operations for Borborema, as Crusader lines up its feasibility studies for the project.

Part of the new management team’s strategy is to rebrand the company that will soon emerge from its ASX hiatus with a change of name to “Big River Gold Ltd” later this month.

In late May, Crusader completed the sale of its Juruena-Novo Astro gold projects to Meteoric Resources for $3m in cash and scrip to entirely focus its efforts on the core Borborema project.

Interestingly, the 50 million fully paid Meteoric shares that the company picked up at 1 cent each in the deal have since doubled in value.

Crusader Chairman Stephen Copulos said: "The sale of Juruena allows the company to improve its cost structure and free up management to accelerate the development of Crusader’s flagship asset, the Borborema gold project.”

“The transaction also allows us to maintain an interest in Juruena through a shareholding in Meteoric Resources which, with its highly professional team, has seen a significant share price increase since the sale was announced.”

The company also recently revealed that it is raising up to $4.1m, before costs, in a rights issue, which will facilitate the optimisation and finalisation of a DFS and BFS for Borborema by the end of this year.

In a show of confidence in the project, the rights issue is partially underwritten to the tune of $2.5m by Mr Copulos and $1m by Pinnacle Capital Finance.

Speaking about his recent appointment and planned direction for Crusader, Mr Richards said: “2019 has seen a fresh start for the company with a change in management and a reinvigorated focus on the large Borborema gold project."

“With the recent sale of non-core assets and a partially underwritten fundraising underway, Crusader’s finances and cost structures have improved and management has been freed-up to accelerate the development of Borborema.”

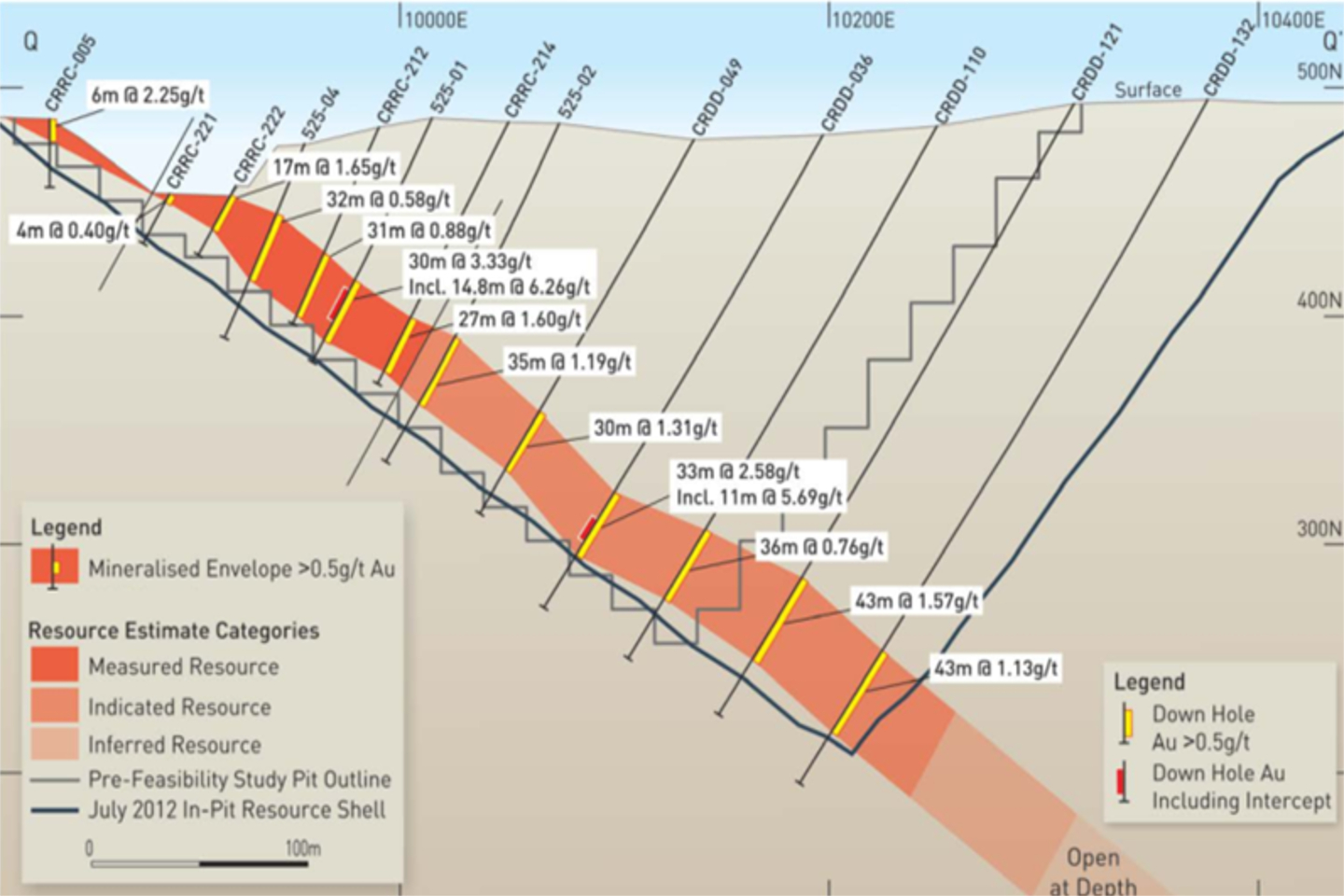

The company has thrown over 95km of drilling at the project since it purchased the property outright in August 2010, from which it grew a JORC-compliant mineral resource of 68.6 million tonnes grading 1.1g/t gold for 2.43 million ounces in mid-2017.

An ore reserve was then optimised from the large mineral resource estimate, with 42.4 million tonnes at 1.18g/t gold estimated for an impressive 1.6 million ounces.

Crusader produced an optimisation study for Borborema in February last year, which outlined a post-tax NPV of USD$118m and an IRR of 31% with free cash flows of USD$243m over an initial mine life of 10 years.

Upfront CAPEX costs were estimated at USD$93m and the operation had a healthy all-in sustaining cost of just over USD$900 per gold ounce that produced good margins, based on a forecast gold price of USD$1,300 per ounce.

The study proposed a conventional 2 million tonne per annum capacity CIL plant, spitting out about 700,000 gold ounces over the decade long initial mine life, at enviable gold recoveries of 93%.

Initial mining activities will concentrate on the upper lens of ore, which contains about 50% of the existing ore reserve at a respectable stripping ratio of just over four to one.

However, with new management comes new eyes and ideas and the company is now looking to enhance these metrics further in several areas, including the use of fixed price quotes, which will help improve the OPEX costs resulting in more confidence and certainty in the development of the operation.

Crusader is hoping to significantly reduce the CAPEX costs at the project and optimise the existing mineral resource by targeting near-surface, higher-grade gold zones that will hopefully lead to a shallower open pit operation and reduce the stripping ratio.

This should have the effect of increasing the gold grades through the mill and potentially improve cash flows in the critical early years of mining.

The company can then pump some of this cash back into the ground at Borborema to potentially extend its tenancy in Brazil.

Crusader believes that Brazil is vastly underexplored for gold and that Borborema in particular, has a lot of blue-sky upside.

The company has already completed preliminary discussions with potential funding partners to underpin the development of the project.

Borborema consists of three mining leases covering a total area of 29 square kilometres including freehold title over the main prospect area of interest, with two permits already granted to allow mining to commence.

The project benefits from a favourable taxation regime, existing on-site facilities and excellent infrastructure such as buildings, grid power, water, sealed roads and is close to major cities and regional centres in this area of Brazil.

The deposit area is located in a very prospective looking region of the country with a semi-arid climate and not in the Amazonian jungles, which means it benefits from year-round access and superb infrastructure as a result.

Crusader is also planning to “dry stack” its tailings above the surface, which minimises the risk of tailings dam collapses – a controversial topic in Brazil at present and a PR nightmare for those companies that have been affected.

This technique makes better use of the scarce water resources in the region and more importantly, will lower the risk to potential investors wanting to get behind the project.

It certainly feels that the Borborema gold project has been kicking around for a while now, however that understates the quality of the resource that Crusader has developed since 2010.

With a singular focus on Borborema and some money in the tin, it appears that Crusader now has its house in order as it moves ever closer to experiencing its day in the sun.

Watch this space.

By Matt Birney

By Matt Birney