Potash plays take punt on product

You can purchase access to this special report or subscribe to Business News.

Subscribe to Business News.

ANALYSIS: WA potash hopefuls may have the backing of some high-profile local mining entrepreneurs, but startup costs and a worldwide product glut are major barriers.

Those following recent activity on the stock market could reasonably form the view that Western Australia is on the verge of a potash boom. In reality, however, the situation could be quite different.

Share prices of companies exposed to the fertiliser, which is high in potassium (hence its name of potash), have been marching higher, largely thanks to work on remote, dry salt lakes in the Pilbara and north-east Goldfields.

{kind=link}

Apart from their common connection at Lake Wells, Salt Lake and Goldphyre share another important asset when it comes to attracting the support of investors – both have the backing of successful WA mining entrepreneurs.

Salt Lake, which started life as a uranium explorer, is the latest in a long line of ASX-listed companies to enjoy the support of Ian Middlemas and Mark Hohnen, men who have made fortunes in earlier bursts of investor enthusiasm for mining.

Goldphyre, which started life as a gold explorer, has attracted the support of Mark Creasy, a rich prospector who has backed a series of winners in nickel and gold but has not previously been known for his interest in potash.

Salt Lake’s share price has risen by 260 per cent during the past six months, from 12 cents to a recent high of 43 cents, before slipping back to 34 cents. That sudden surge helped trigger a stampede for a share issue, which set out to raise $5.2 million but instead attracted $8.4 million.

Goldphyre has an even more impressive share price record, up 660 per cent over 12 months to a recent high of 11.5 cents, but with a less ambitious fundraising target of $1.1 million for its work at Lake Wells – though applications for shares outnumbered what was on offer.

Other Perth-based potash hopefuls with international assets have shared in the revitalised interest in the fertiliser, including:

• Danakali, which has a promising project in the North African country of Eritrea, raising $5.5 million in late March;

• Plymouth Minerals, which has assets in another African county, Gabon, raised $3 million; and

• Elemental Minerals, which has a potentially big project in the Republic of Congo and has reportedly attracted the interest of private equity funds offering $US40 million to start development of its Kola project.

Then there’s the case of a Melbourne-based potash favourite, the Owen Hegarty-led Highfield Resources. Its share price soared to $2.08 earlier this year before crashing back to $1.17 when it was hit by possible government approval problems at its Muga project in Spain.

Most of the projects in the exploration and planning stages share a common geology involving the concentration of salts, including potassium chloride and sodium chloride (traditional table salt) in lakebeds as they have dried out.

The potassium has generally been carried into the salt lake down ancient drainage channels, which have also been the conduits for other minerals, such as uranium, which has been eroded off surrounding rock.

Salt Lake Potash, for example, changed its name late last year from Wildhorse Energy, though its principal area of interest remained Lake Wells.

In some cases the ancient lakebeds are now hundreds (or thousands) or metres from the surface, which is how potash mining is undertaken in Germany and Canada, or they are close to the surface, which is how potash is produced at the Dead Sea in Israel.

As encouraging as it may be to see funds flow into a promising part of the mining industry, there are potentially more negative forces at work in potash than the positive forces exploration companies are so eager to mention in their presentations.

Internationally, there is no shortage of potash. As with many other commodities, the potash market is awash with product, with the result being lower prices for the fertiliser, in its many forms, and mine closures in a number of countries, most notably Canada.

Big mining companies have become wary of potash just as smaller companies seek a way into a business that is a classic bulk commodity, meaning that it generally requires high levels of initial capital to fund developments plus reliable access to railway systems and ports – much like iron ore and coal.

BHP Billiton, the world’s biggest resources company and a bulk-commodity specialist, has been trying to find a way into potash for the past 10 years, first by attempting (and failing thanks to Canadian government objections) to acquire Potash Corporation of Saskatchewan, and more recently by trying to develop its own Jansen potash mine in Canada.

Whether BHP Billiton ever becomes a significant producer of potash is questionable with early-stage work at Jansen slowed from an annual investment of more than $US300 million to a planned $US200 million this year.

The cash required to bring a big potash project into production is one of the hurdles confronting most potential producers, though some argue that it is possible to avoid the sort of deep developments seen in Canada and Germany by focusing on surface mining, which is how potash is produced in Israel and might one day be produced at Lake Wells or other sites in WA.

High initial costs also look like delaying a big potash development planned for northern Britain. The first phase of a deep mine planned by UK-based Sirius Minerals near Whitby in North Yorkshire has an estimated cost of more than £2.5 billion ($4.7 billion) – a heavy lift with the price of potash low and showing no sign of a recovery.

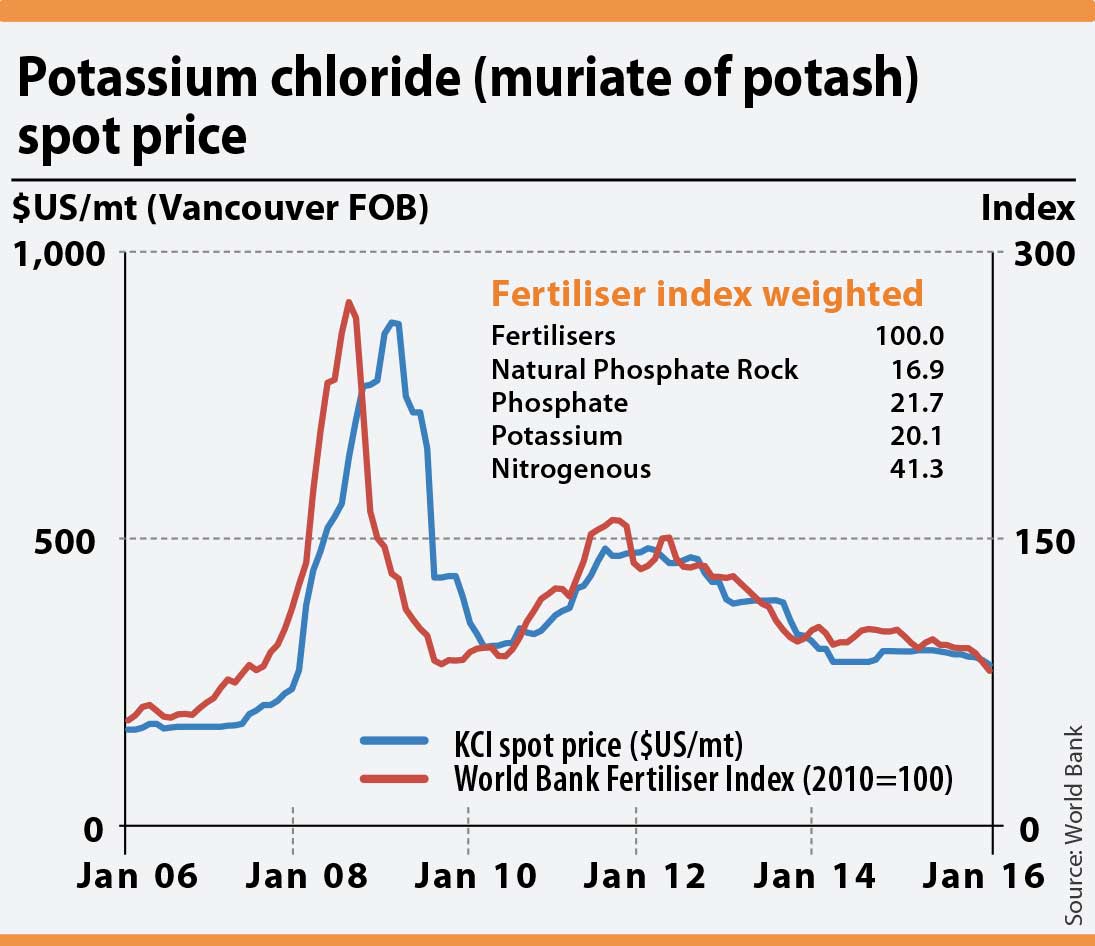

Potash promoters, understandably, tend to skip lightly over the question of the potash price and can be guilty of obscuring the issue by claiming to have either ultra-low costs or a focus on the production of a premium quality form of potash – a product called sulphate of potash (SoP) rather than lower value muriate of potash (MoP).

Some farmers prefer SoP because it contains beneficial sulphur and less chloride. But it is more expensive and farmers are notoriously careful with their cash or, in the developing world, cannot afford to buy anything other than MoP.

The quality difference and complexity of production mean that SoP sells today for around $US650 a tonne. MoP fetches around $US280/t, which is down 40 per cent on the $US470/t of three years ago.

Like many other commodities, including iron ore, coal and nickel, potash is not in short supply. It is actually suffering from the same problems of producers getting ahead of demand partly because of the promise of a ‘green revolution’ driven by Chinese food demand.

Projections of future potash consumption point to a 60 per cent increase in demand over the next 15 years; and while that might sound impressive it actually represents relatively modest growth of 4 per cent a year, which is not far above forecast overall global economic growth of between 3 per cent and 3.5 per cent a year.

Into this mix of high costs, low prices, slow demand growth, over-production and mine closures, has arrived the stock market boom in WA potash hopefuls.

It is possible remote sites such as Lake Wells will one day support a potash industry, but for that to happen the infrastructure (railways and roads) need to be developed, a production system proved, and customers found for a product already in abundant supply.

However news from the international market is not promising.

• Canada’s Potash Corporation recently suffered an earnings downgrade by that country’s leading investment bank, CIBC.

• The Bank of Montreal’s potash expert, Joel Jackson, told a conference last month that potash prices have probably not bottomed and could continue to fall.

• US investment bank Morgan Stanley Wealth Management is forecasting an oversupply of potash in the short to medium term.

• German potash company K+S expects worldwide demand in 2016 to remain at around 64 million tonnes a year, leading to intense competition and a significant drop in the average price.

The tough outlook of supply exceeding demand has forced Potash Corporation to mothball three of its mines, including the $US1.5 billion Piccadilly mine in New Brunswick, which only started production 18 months ago.

WA’s salt lake-focused potash hopefuls argue that they’re different because the mining method would be simpler (surface mining or underground solution mining), and that they will produce high-value SoP.

It might happen, and it would be welcome, as potash would be a new industry for WA.

But a lot needs to go right before WA becomes a significant source of potash and there’s no doubt that the world’s existing big producers would make life very difficult for any new entrants – as has happened to BHP Billiton in Canada.